Inflation and the Impact on Timing CPP Benefits

.webp)

While there has been little reason to embrace the high inflation of today, there may be a silver lining for certain government benefits. Higher inflation means higher Canada Pension Plan (CPP) benefits and the outcome can be especially significant the longer you wait to begin. The standard age to start CPP is 65, but you can begin as early as age 60. In fact, most people start early.1 However, if you have yet to apply for CPP, it may be an opportune time to revisit the timing decision.

How Does Inflation Impact CPP Benefits?

CPP payments are impacted by inflation in two ways. First, like most government benefits, they are indexed to the consumer price index (CPI). The CPP uses the measure of CPI over the 12-month period ending October of the previous year and makes adjustments the following January 1. Second, CPP is also adjusted based on the year’s maximum pensionable earnings (YMPE), an amount indexed to wage inflation. Over recent times, increases to the YMPE have been significant: 4.94 percent in 2021 and 5.36 percent in 2022. This was largely due to the pandemic when the services industry suffered and fewer people worked in lower-paying jobs, pushing up average weekly earnings.2

The Timing Decision to Take CPP

If you start receiving CPP benefits before age 65, payments will decrease by 0.6 percent each month to a maximum of 36 percent (at age 60). If you start after 65, payments increase by 0.7 percent each month, to a maximum of 42 percent (at age 70 or after). However, by waiting to take benefits, CPP amounts can grow based on inflation, and this is further enhanced by the increased benefit of starting later.

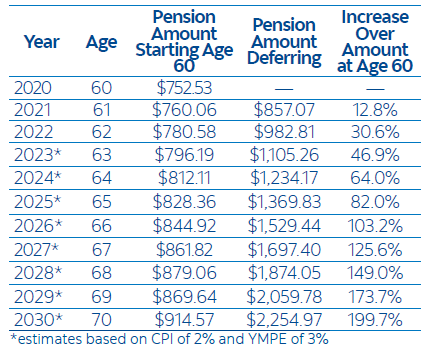

A recent analysis shows the potential impact. It looks at an individual who started CPP at age 60 in January 2020, with a decreased benefit of 36 percent (0.6% X 60 months). Assuming the maximum CPP pension amount of $1,175.83 in 2020, she received $752.53. Had she waited a year and started at age 61, she would have received $857.07 (a 28.8 percent decreased benefit from $1,203.75). If she waited until age 62, she would have received $982.81, or 30.6 percent more than she would have received at age 60.

Just how significant is the difference? The table shows the potential increase over time, based on actual 2021 and 2022 figures. It assumes future CPI adjustments (after 2022) of two percent and maximum retirement pension increases of three percent based on existing actuarial assumptions. By these calculations, at age 90 an individual would have a cumulative pension that is 83 percent larger by waiting to start at age 70, compared to starting early at 60.

Of course, many factors should be considered as you decide when to begin CPP, including expected longevity, the impact of income-tested benefits, the need for income, and more. However, the impact of inflation may be one compelling reason for individuals to consider waiting to begin CPP benefits.